24 May 2024

Travis Tucker, CFA

HSBC Asset Management, Research & Insights Senior Manager

Cathrine De Coninck Lopez

HSBC Asset Management, Global Head of Responsible Investment

Learning About ESG is an educational series that connects environmental, social and governance topics with investing.

Join us each issue to see how global developments can have implications for investors. The better we understand ESG, the bigger the role it can play in our everyday lives – and investment portfolios – contributing to a better world.

Today we finance a number of industries that significantly contribute to greenhouse gas emissions. We have a strategy to help our customers to reduce their emissions and to reduce our own. For more information visit www.hsbc.com/sustainability.

At the centre of this transition are people whose livelihoods will be affected by the momentous shift - from workers facing redundancy, to consumers impacted by energy prices and local economies that depend on oil revenue. A just transition will ensure that individual countries, communities or workers don’t bear a disproportionate burden as we shift to a low-carbon economy. This requires supporting communities reliant on carbon-intensive sectors to adapt their industries and train the workforce accordingly. Without this support, negative social outcomes can damage economies.

Emerging markets are an important element of this story. Over the past few decades, a substantial portion of carbon-intensive industrial activity has been relocated from developed to emerging countries. This has been largely due to lower production costs and less scrutiny over environmental issues. Fast-growing emerging economies in Asia are now driving emissions growth – with the region accounting for roughly half of global emissions.

Of course, environmental damage must be limited globally, which requires substantial change. While yet to be fulfilled, USD100 billion per year committed in climate finance to developing countries through the COP climate summits can support the objectives of a just transition, by helping facilitate the industrial change needed in these markets.

Achieving a just transition has important financial implications for investors. Social issues related to shifting industries and job opportunities poses risks to political structures and economic growth. Furthermore, higher levels of morale in the labour market fosters better productivity, as supported by a prominent study of stock market returns from 1984 to 2009[@learning-about-esg-2-1], with materially better performance by companies with high employee satisfaction.

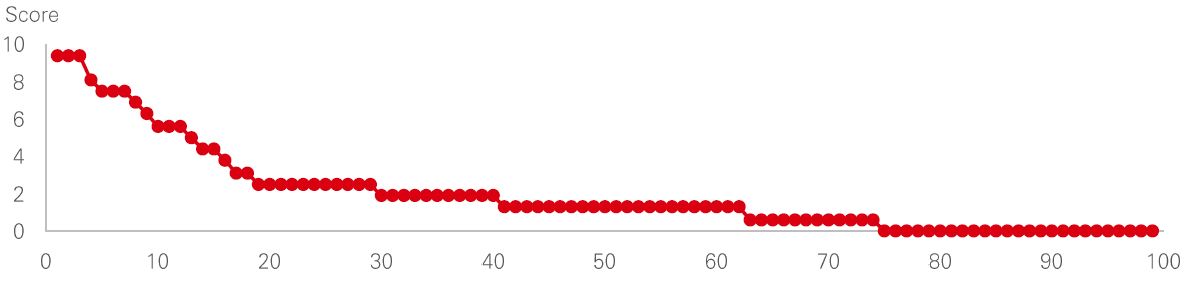

Clearly the oil industry is key to a just transition. Yet, of 100 companies assessed globally, roughly a quarter received a score of zero in an analysis of efforts to support a just transition. Societal and financial implications support growing investor scrutiny on this.

Oil and gas company 2023 just transition assessment scores (out of 20)

Source: HSBC Asset Management, World Benchmarking Alliance Climate and Energy Benchmark Report, 29 June 2023.

A portfolio of the top 25 companies to work for, as ranked by the Great Place to Work Institute, has significantly outperformed the broader equity market over the last decade. While such a concentrated portfolio creates inherent biases, it aligns with prior academic research demonstrating that companies with higher employee morale and a more positive impact on communities in which they operate achieve better productivity and performance.

Similarly, MSCI research delved into the performance impacts of the individual components of ESG (environmental, social and governance considerations). Analysing returns over the last decade, stocks with top quintile ‘S’ scores outperformed their bottom quintile peers, with the outperformance being more significant than equivalent comparisons for ‘E’ or ‘G’ scores. The performance advantage has been particularly evident in recent years, perhaps reflecting improved productivity from those companies that invested in their staff during the pandemic.

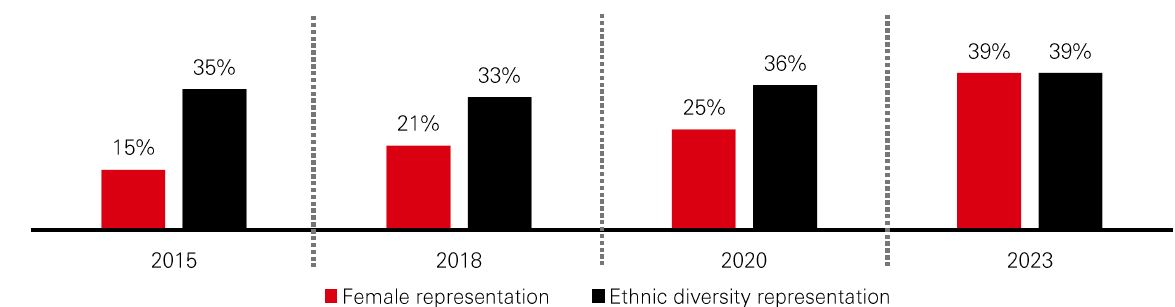

When considering company morale and impacts on the communities in which they operate, whether company leadership reflects those communities can likewise be an indicator for performance and productivity.

Various studies demonstrate a positive link between diversity and company performance. That is, companies with more diverse leadership have delivered better results, which is intuitive given the proven benefits of decision-making that incorporates different perspectives, such as those most relevant to local communities and customers. Per the chart below, the most diverse firms have seen an increase in their levels of outperformance, measured by profitability, over the years.

Cause and effect for this outperformance can be complicated by a combination of factors. Nonetheless, data broadly support the argument that societal considerations are as important as any ESG pillars. Accordingly, making such considerations a priority is in the best interests of long-term investors.

Greater diversity on executive teams aligns with financial outperformance

Difference in likelihood of outperformance of 1st versus 4th quartile

Past performance is not an indicator of future returns. Source: McKinsey & Company, December 2023.

Inequality, another important societal issue, has increasingly been a topic of discussion due to strikes and other large-scale labour action in recent years. Income and wealth inequality has been on the rise almost everywhere since the 1980s and is now at its most severe since the early 20th century.

This points to a need for improvement in workforce treatment and poverty reduction. In the absence of progress, we should expect more systemic issues such as breakdowns in social cohesion and disruptions to political stability. This will create turbulence in financial systems and hinder economic growth.

Any discussion of investment in the workforce today would be incomplete without mentioning developments in artificial intelligence. Rapid progress in the technology has contributed to much angst around societal risks, from data privacy to the widescale elimination of human jobs. Accordingly, discussions among regulators, industry leaders and academics on these matters have picked up steam.

The EU is taking significant strides in formally addressing concerns, with a proposed AI Act outlining a comprehensive governance framework around AI systems, extending from product development to data privacy. Other steps will surely follow.

Regulations aside, while AI will certainly improve automation and reduce the need for certain human tasks, it will also enhance human productivity. Companies best positioned to succeed will prioritise training their workforces with the relevant skills to work alongside new AI capabilities and increase output.

All of this discussion leads to the conclusion that incorporating social considerations within an ESG framework is in line with investors’ interests. For those seeking investment solutions focused more specifically on social considerations, we expect momentum to build with relevant offerings given evidence supporting potential performance benefits. Even more importantly, growing demand along with pressure from both investors and asset managers can help drive progress, including in laggard areas such as oil & gas.

ESG: A set of Environmental, Social and Governance criteria that investors can apply to analyse and identify material risks and growth opportunities in investments.

Just transition: Seeks to ensure that the benefits of a green economy transition are shared widely, while also supporting those who stand to lose economically.

This document or video is prepared by The Hongkong and Shanghai Banking Corporation Limited (‘HBAP’), 1 Queen’s Road Central, Hong Kong. HBAP is incorporated in Hong Kong and is part of the HSBC Group. This document or video is distributed and/or made available by HSBC Bank Canada (including one or more of its subsidiaries HSBC Investment Funds (Canada) Inc. (“HIFC”), HSBC Private Investment Counsel (Canada) Inc. (“HPIC”) and HSBC InvestDirect division of HSBC Securities (Canada) Inc. (“HIDC”)), HSBC Bank (China) Company Limited, HSBC Continental Europe, HBAP, HSBC Bank (Singapore) Limited, HSBC Bank Middle East Limited (UAE), HSBC UK Bank Plc, HSBC Bank Malaysia Berhad (198401015221 (127776-V))/HSBC Amanah Malaysia Berhad (20080100642 1 (807705-X)), HSBC Bank (Taiwan) Limited, HSBC Bank plc, Jersey Branch, HSBC Bank plc, Guernsey Branch, HSBC Bank plc in the Isle of Man, HSBC Continental Europe, Greece, The Hongkong and Shanghai Banking Corporation Limited, India (HSBC India), HSBC Bank (Vietnam) Limited, PT Bank HSBC Indonesia (HBID), HSBC Bank (Uruguay) S.A. (HSBC Uruguay is authorised and oversought by Banco Central del Uruguay), HBAP Sri Lanka Branch, The Hongkong and Shanghai Banking Corporation Limited – Philippine Branch, and HSBC FinTech Services (Shanghai) Company Limited (collectively, the “Distributors”) to their respective clients. This document or video is for general circulation and information purposes only.

The contents of this document or video may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This document or video must not be distributed in any jurisdiction where its distribution is unlawful. All non-authorised reproduction or use of this document or video will be the responsibility of the user and may lead to legal proceedings. The material contained in this document or video is for general information purposes only and does not constitute investment research or advice or a recommendation to buy or sell investments. Some of the statements contained in this document or video may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. HBAP and the Distributors do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document or video has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed are based on the HSBC Global Investment Committee at the time of preparation, and are subject to change at any time. These views may not necessarily indicate HSBC Asset Management‘s current portfolios’ composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients’ objectives, risk preferences, time horizon, and market liquidity.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. Past performance contained in this document or video is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Investments are subject to market risks, read all investment related documents carefully.

This document or video provides a high level overview of the recent economic environment and has been prepared for information purposes only. The views presented are those of HBAP and are based on HBAP’s global views and may not necessarily align with the Distributors’ local views. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. It is not intended to provide and should not be relied on for accounting, legal or tax advice. Before you make any investment decision, you may wish to consult an independent financial adviser. In the event that you choose not to seek advice from a financial adviser, you should carefully consider whether the investment product is suitable for you. You are advised to obtain appropriate professional advice where necessary.

The accuracy and/or completeness of any third party information obtained from sources which we believe to be reliable might have not been independently verified, hence Customer must seek from several sources prior to making investment decision.

Important Information about HSBC Global Asset Management (Canada) Limited (“AMCA”)

HSBC Asset Management is a group of companies, including AMCA, that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings plc. AMCA is a wholly owned subsidiary of, but separate entity from, HSBC Bank Canada.

Important Information about HSBC Investment Funds (Canada) Inc. (“HIFC”)

HIFC is the principal distributor of the HSBC Mutual Funds and offers the HSBC Mutual Funds and/or the HSBC Pooled Funds through the HSBC World Selection® Portfolio service. HIFC is a subsidiary of AMCA, and indirect subsidiary of HSBC Bank Canada, and provides its products and services in all provinces of Canada except Prince Edward Island. Mutual fund investments are subject to risks. Please read the Fund Facts before investing.

®World Selection is a registered trademark of HSBC Group Management Services Limited.

Important Information about HSBC Private Investment Counsel (Canada) Inc. (“HPIC”)

HPIC is a direct subsidiary of HSBC Bank Canada and provides services in all provinces of Canada except Prince Edward Island. The Private Investment Counsel service is a discretionary portfolio management service offered by HPIC. Under this discretionary service, assets of participating clients will be invested by HPIC or its delegated portfolio manager, AMCA, in securities, including but not limited to, stocks, bonds, mutual funds, pooled funds and derivatives. The value of an investment in or purchased as part of the Private Investment Counsel service may change frequently and past performance may not be repeated.

Important Information about HSBC InvestDirect (“HIDC”)

HIDC is a division of HSBC Securities (Canada) Inc., a direct subsidiary of, but separate entity from, HSBC Bank Canada. HIDC is an order execution only service. HIDC will not conduct suitability assessments of client account holdings or of the orders submitted by clients or from anyone authorized to trade on the client’s behalf. Clients have the sole responsibility for their investment decisions and securities transactions.

Important Information about the Hongkong and Shanghai Banking Corporation Limited, India (“HSBC India”)

HSBC India is a branch of The Hongkong and Shanghai Banking Corporation Limited. HSBC India is a distributor of mutual funds and referrer of investment products from third party entities registered and regulated in India. HSBC India does not distribute investment products to those persons who are either the citizens or residents of United States of America (USA), Canada, Australia or New Zealand or any other jurisdiction where such distribution would be contrary to law or regulation.

The following statement is only applicable to HSBC Bank (Taiwan) Limited with regard to how the publication is distributed to its customers: HSBC Bank (Taiwan) Limited (“the Bank”) shall fulfill the fiduciary duty act as a reasonable person once in exercising offering/conducting ordinary care in offering trust services/ business. However, the Bank disclaims any guarantee on the management or operation performance of the trust business.

The following statement is only applicable to PT Bank HSBC Indonesia (“HBID”): PT Bank HSBC Indonesia (“HBID”) is licensed and supervised by Indonesia Financial Services Authority (“OJK”). Customer must understand that historical performance does not guarantee future performance. Investment product that are offered in HBID is third party products, HBID is a selling agent for third party product such as Mutual Fund and Bonds. HBID and HSBC Group (HSBC Holdings Plc and its subsidiaries and associates company or any of its branches) does not guarantee the underlying investment, principal or return on customer investment. Investment in Mutual Funds and Bonds is not covered by the deposit insurance program of the Indonesian Deposit Insurance Corporation (LPS).

THE CONTENTS OF THIS DOCUMENT OR VIDEO HAVE NOT BEEN REVIEWED BY ANY REGULATORY AUTHORITY IN HONG KONG OR ANY OTHER JURISDICTION.

YOU ARE ADVISED TO EXERCISE CAUTION IN RELATION TO THE INVESTMENT AND THIS DOCUMENT OR VIDEO. IF YOU ARE IN DOUBT ABOUT ANY OF THE CONTENTS OF THIS DOCUMENT OR VIDEO, YOU SHOULD OBTAIN INDEPENDENT PROFESSIONAL ADVICE.

© Copyright 2023. The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED.

No part of this document or video may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

Important information on sustainable investing

“Sustainable investments” include investment approaches or instruments which consider environmental, social, governance and/or other sustainability factors (collectively, “sustainability”) to varying degrees. Certain instruments we include within this category may be in the process of changing to deliver sustainability outcomes.

There is no guarantee that sustainable investments will produce returns similar to those which don’t consider these factors. Sustainable investments may diverge from traditional market benchmarks.

In addition, there is no standard definition of, or measurement criteria for sustainable investments, or the impact of sustainable investments (“sustainability impact”). Sustainable investment and sustainability impact measurement criteria are (a) highly subjective and (b) may vary significantly across and within sectors.

HSBC may rely on measurement criteria devised and/or reported by third party providers or issuers. HSBC does not always conduct its own specific due diligence in relation to measurement criteria. There is no guarantee: (a) that the nature of the sustainability impact or measurement criteria of an investment will be aligned with any particular investor’s sustainability goals; or (b) that the stated level or target level of sustainability impact will be achieved.

Sustainable investing is an evolving area and new regulations may come into effect which may affect how an investment is categorised or labelled. An investment which is considered to fulfil sustainable criteria today may not meet those criteria at some point in the future.